Small makhana processors often face one big roadblock: the makhana processing plant cost more than they can afford upfront. Agri-fintech platforms are changing that. Instead of complicated business loans, they offer direct financing for essential processing machines like roasters, graders, and packers. The result? Access to advanced machinery, faster, better product quality, and a real plan for scaling up. It’s not just easier credit. It’s a way to turn loan-approved makhana processing equipment into a stable, income-generating business.

The Reality: Why Loan-Approved Equipment Is a Must

Even a basic makhana processing setup costs ₹5–15 lakhs. That’s out of reach for most SHGs, FPOs, and small rural businesses. They are stuck with manual work, slow, inconsistent, and hard to scale. Quality suffers. So do profits.

Banks Drag Their Feet. Fintech Doesn’t.

- Traditional banks see these small units as risky. The paperwork alone takes weeks.

- That’s where agri-fintech platforms are changing the game.

- They offer faster, smaller loans, specifically for processing equipment.

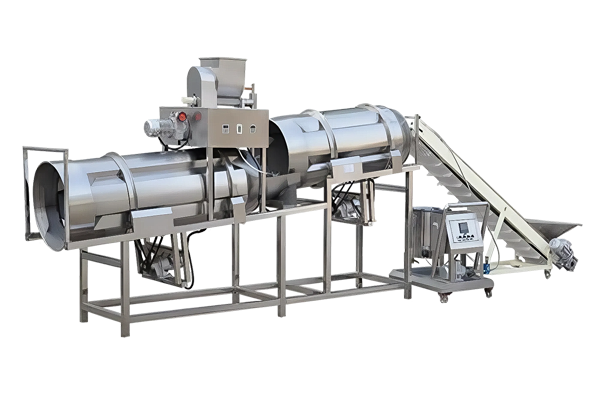

What These Loans Cover

- Roasters, crackers, poppers, graders, polishers, packers, the full line.

- All are set up with food-grade stainless steel, so hygiene and compliance aren’t a concern.

- It’s not partial funding. It’s the full setup, just made possible in steps.

What This Means on the Ground

- Machines bring consistency. Labor drops, output rises.

- Better quality means better market prices. That directly improves margins.

- More local jobs, more sustainable village units, and a real seat at the table in India’s food economy.

What Counts as Loan-Approved Makhana Equipment

Rural entrepreneurs investing in loan-approved makhana processing equipment can now access financing more easily if the machines meet the right criteria. Automatic roasters, grading units, and packaging systems that are GST-compliant, invoice-ready, and aligned with schemes like PMFME, NABARD, and AIF typically qualify. Lenders also favor machinery with documented use in the field and available local service support.

Agri-fintech platforms and NBFCs are more confident funding setups that show cost transparency, low maintenance, and government compliance. For rural FPOs and SHGs, that means faster access to loans, better processing capacity, and lower manual effort without waiting for subsidy delays. It’s a practical path to modernize and grow makhana businesses with reduced upfront burden.

Case Study: How a Small FPO in Bihar Got ₹6.5 Lakh Financing for Makhana Setup

If you are running a rural food processing machine unit, getting financing for an affordable makhana machine for rural entrepreneurs is no longer a shot in the dark. Banks and NBFCs are far more open to funding when your equipment ticks a few clear boxes.

Here is the thing: loan-approved makhana processing equipment that comes with GST billing, official invoices, and aligns with government schemes like PMFME, NABARD, and AIF tends to get approved quickly. Add a local service backup and proof that others have used the same setup successfully, and lenders feel more confident. It’s not just about what you buy, but how well it fits into a system that’s already working.

Read More: How BIHAR Farmers Are Doubling Makhana Output with Affordable Machines

Loan vs. Makhana Equipment Cost Breakdown

Let’s break it down. If you are building a rural food processing machine unit that’s both efficient and loan-worthy, here’s what matters: the loan-approved makhana processing machine you choose, the work they do, and how much they will cost. The setup below is lean, practical, and focused on what gets results: roasting, grading, coating, and packaging.

| Machine | Purpose | Capacity | Estimated Cost (₹) | Loan Eligibility Notes |

|---|---|---|---|---|

| Automatic Makhana Roaster | Uniform roasting of raw makhana | 50–100 kg/hr | ₹2.5 – ₹4.5 lakh | PMFME/NABARD-ready if GST invoice + local support |

| Grading Machine | Size-based sorting (S/M/L) | 100–200 kg/hr | ₹1.5 – ₹2.5 lakh | Essential for quality-based pricing |

| Flavor Coating Machine | Adds masala, ghee, or jaggery coating | 50–80 kg/hr | ₹1.2 – ₹2 lakh | Qualifies under value-addition funding |

| Semi-Automatic Packaging Unit | Weighing, sealing, and basic labeling | 200–400 pouches/hr | ₹90,000 – ₹1.5 lakh | Supports retail-ready micro-enterprise setups |

| Total Estimate | For 50–100 kg/hr pilot setup | — | ₹6.2 – ₹10.5 lakh | EMI-friendly under PMFME/NABARD/AIF |

Loan-Approved Makhana Machine: Key Features

Loan-approval makhana processing equipment starts with what’s on your shop floor. If your affordable makhana machine for rural entrepreneurs doesn’t look reliable or compliant, lenders hesitate. They need proof that your setup can run safely and make money. Here’s what features matter:

-

Invoice-ready, GST-billed machines

These aren’t just formalities. A proper invoice with GST creates cost clarity. It’s what lenders and government schemes want to see. Without it, your loan file might not even get off the desk.

-

After-sales service guarantee

Loan-approved makhana processing equipment break. What matters is who fixes them and how fast. A supplier who offers AMC or local repair backup makes your setup reliable. That reduces downtime and makes lenders more willing to bet on you.

-

Government scheme compatibility (PMFME, AIF)

Schemes like PMFME or AIF aren’t just paperwork; but they are the checklists. Loan-approved makhana processing equipment that meets their specifications is easier to approve, especially when subsidies are involved. It also means NBFCs and fintech lenders are more likely to say yes.

-

So what does all this add up to?

It means better access to small-ticket loans. Rural entrepreneurs, especially in areas like loan-approved makhana processing equipment, can finally scale with confidence. And not just start something, but keep it running and growing.

If you’re applying for a government-backed loan, check whether your unit qualifies under the PM-FME Scheme.

Ready to Launch Your Makhana Unit with Financing?

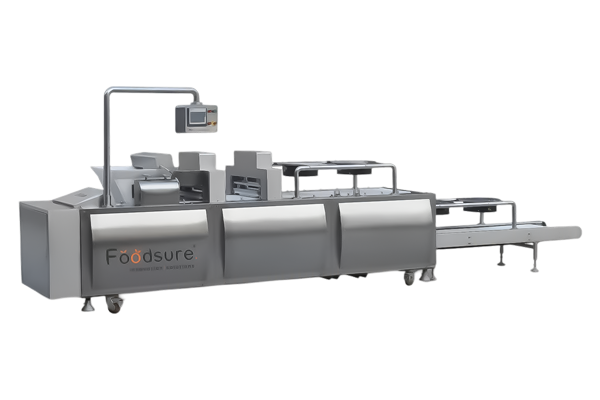

Starting a loan-approved makhana processing equipment unit doesn’t have to mean waiting years to save up. With Foodsure Machines, you get GST-billed, loan-ready equipment, clear paperwork, and support that actually helps, from expert financing guidance to connections with lenders. The kit is compliant with PMFME and designed to scale as you grow. It’s a practical, low-risk way for rural entrepreneurs to access funding and kickstart their Makhana business with confidence. Want Help Setting Up a Finance-Backed Makhana Unit?

FAQ

1. What types of Makhana processing machinery qualify for rural microloans?

Machines that come with proper GST billing, verified invoices, and align with PMFME or NABARD norms usually qualify. Think automatic roasters, graders, or packaging units from credible suppliers, anything that’s compliant and documented properly.

2. How does agri-fintech help rural entrepreneurs access loans for Makhana machinery?

These platforms make it easier to get small loans fast. They offer simple paperwork, fair interest rates, and help FPOs or SHGs fill financing gaps without waiting for banks to move.

3. What key features increase the chances of machinery being finance-eligible?

Lenders look for clarity. Machines with transparent pricing, warranty-backed service, and government-scheme alignment have a better shot at quick loan approvals.

4. What benefits do rural entrepreneurs gain by using microloans for Makhana machinery?

They get to upgrade without the wait, better output, less manual work, and a real shot at scaling profitably, all without putting up big money upfront.

5. What subsidy is available for loan-approved Makhana processing equipment?

Most government food-processing schemes offer 35–50% capital subsidy on approved Makhana machinery.

6. How can I start a business using loan-approved Makhana processing equipment?

Apply for machinery loans under food-processing schemes and set up a small FSSAI-registered processing unit.

7. Is investing in loan-approved Makhana processing equipment profitable?

Yes—high demand and low raw material cost make processing units strongly profitable.

8. How much does processed Makhana sell for per kg after using approved equipment?

Branded processed Makhana typically sells for ₹500–₹1,000 per kg depending on quality.

9. Which loan offers around 50% subsidy for Makhana processing equipment?

Schemes like PMFME often provide up to 50% subsidy on approved food-processing machinery.

10. What is the food-processing loan scheme for Makhana equipment?

The PMFME and similar schemes offer loans plus subsidies for machinery and unit setup.

11. How much does 100 g of processed Makhana cost when produced with loan-approved equipment?

Retail packs usually range from ₹50–₹120 per 100 g depending on flavor and brand.

12. How can loan-approved equipment help earn ₹1 lakh/month from Makhana processing?

By scaling roasting, grading, and packaging operations to supply wholesalers and online markets.